Which Country Will Win the 2025 Microchip Supremacy Race

Insights | 15-01-2025 | By Paul Whytock

In an increasingly microchip-enabled world, he who has the best and most advanced microchips, along with a large, stable supply of bread-and-butter devices, can steal the lead in the power plays that influential countries inflict on each other.

Microchip supremacy enhances economic ability, strengthens communication and computing systems, is an essential fuel in the relentless drive towards military supremacy and enhances a country's productivity in manufacturing, farming and medical science and the development of artificial intelligence (AI).

Key Things to Know:

- Taiwan's Dominance in Chip Production: Taiwan, led by TSMC, supplies over 90% of the global market for advanced microchips, giving it significant influence in global technology and security dynamics. However, political tensions with China create economic and security challenges for the island.

- US-China Rivalry and Export Controls: The US is actively restricting China's access to advanced semiconductor technologies to prevent its military advancements, enforcing export controls and collaborating with allies like Japan and the Netherlands to limit key chipmaking equipment sales to China.

- Europe and UK Lagging but Investing: While Europe and the UK have strong R&D capabilities, they lag in manufacturing capacity and self-sufficiency. Both regions have introduced significant funding initiatives, such as the EU's €43 billion chip plan and the UK's focus on compound semiconductors and chip design.

- Future Chip Supremacy Outlook: Taiwan, in cooperation with the US and Japan, is poised to maintain chip leadership due to their collaborative manufacturing expansions and cutting-edge technologies, while China and Russia face ongoing challenges in achieving chip self-sufficiency.

So how are major countries and continents that desire such supremacy doing? Let's start with the major player, the keystone element that influences the global chip market, Taiwan.

Taiwan: Global Leader in Advanced Microchip Production

In a nutshell, Taiwan is as the world's leading producer of advanced chips and supplies over 90 percent of the global market share, giving it tremendous influence in the chip supremacy stakes. But it's not all plain sailing for the likes of TSMC, Winbond and other major Taiwanese fabs.

For instance, despite the clear political friction between Taipei and Beijing, Taiwan supplies essential components to Chinese industries. These sales may boost Taiwan's economy, but they also enhance China's military capabilities, which raises the security threat to Taiwan. According to Taiwan's Ministry of Economic Affairs, in 2023, China accounted for 35% of its total exports.

So, in effect, Taiwan is firmly wedged between its economic interests in China and its security and business ties with the United States.

A continuing difficulty for Taiwan is its exclusion from global semiconductor policy decision-making. However, in the long -term this hasn't stopped the country being a massive influence in the global chip market, so its exclusion may actually be more to the detriment of the G7 countries.

During the assembly of the G-7 Semiconductors Point of Contact Group in 2024 a real effort was made by major global powers to coordinate semiconductor-related R&D and crisis management. The relevance of these matters to Taiwan is obvious, yet Taiwan is denied a recognised channel in which it can contribute in these discussions.

Back to those political frictions between Beijing and Taipei, which often result in some military sabre-rattling exercises by the Chinese military, let's get one thing clear; a full-scale invasion by China into Taiwan would be disastrous for Taiwan and the rest of the world.

TSMC plans to increase production capacity at its Nanjing, China facility. (Image credit: TSMC)

This view is supported by US Commerce Secretary Gina Raimondo who has said that a seizure of a chip producer like TSMC would be "absolutely devastating" to the American economy. "The United States buys 92% of its leading edge chips from TSMC in Taiwan."

Last month, Raimondo announced the Commerce Department would award TSMC's American unit a $6.6 billion subsidy for its most advanced semiconductor production in Phoenix, Arizona and up to $5 billion in low-cost government loans.

TSMC agreed to expand its planned investment by $25 billion to $65 billion and to add a third Arizona fab by 2030.

There are also other possible situations and rumours that significantly impact the relationship between Beijing and Taipei, and perhaps one of the most speculative of these is that Taiwan would self-destruct its own fabrication plants if China invaded. This scenario was stated last year when the US Army War College published a paper suggesting the Taiwanese government might give TSMC's chip fabs their own self-destruct systems. It's also a theory that has been muted by a number of influential figures in the island's semiconductor businesses.

Now, blowing up TSMC for example wouldn't sound the death knell for humanity but it would cause global chaos given TSMC huge global market share of 62%.

So, Taiwan plays a major role in the chip ambitions of both the US and China.

US-China Microchip Rivalry and Export Restrictions

Where does this put the US regarding its often uneasy relationship with China? Washington's worries are simple. They don't want China's military ability to surpass the US military in terms of overall power. The second is that China could use US technology to do so.

President Xi Jinping of China has decreed the country's military must become world-class in the next 25 years, although what world-class actually means is unclear. A big part of that would mean developing autonomous weaponry, including hypersonic missiles and using artificial intelligence (AI) for a range of applications, including electronic warfare.

It is unclear how close China is to achieving this goal. According to the US department of defence's annual report on China's military power, the PLA is "pursuing next-generation combat capabilities … defined by the expanded use of artificial intelligence and other advanced technologies at every level of warfare".

By Office of U.S. Commerce Secretary - https://twitter.com/SecRaimondo/status/1395789309580648448, Public Domain, Link

But while China is a world-leader in certain AI applications, such as facial recognition, its domestic industry is not yet able to produce the most advanced semiconductors that power these technologies. So Chinese businesses and its military rely on imports to gain access to the advanced chips.

The US wants to turn off that tap. What measures has the US taken so far?

In October, the Biden administration imposed a sweeping set of export controls, targeting China's access to US-origin semiconductors and their related products. Businesses and individuals in China are now unable to buy advanced chips and chipmaking technology from US suppliers without the seller obtaining a specific licence from the US government.

The US has strengthened these controls by persuading the Netherlands and Japan to curb exports of technology used in the production of chips. Both countries were targeted because they are home to some of the world's most advanced chip manufacturing technologies, including the Netherlands' ASML. ASML is the only company that can provide the latest generation of photolithography scanner equipment, which is used to etch microscopic circuits on silicon wafers.

Both Japan and the Netherlands have now agreed with US policy.

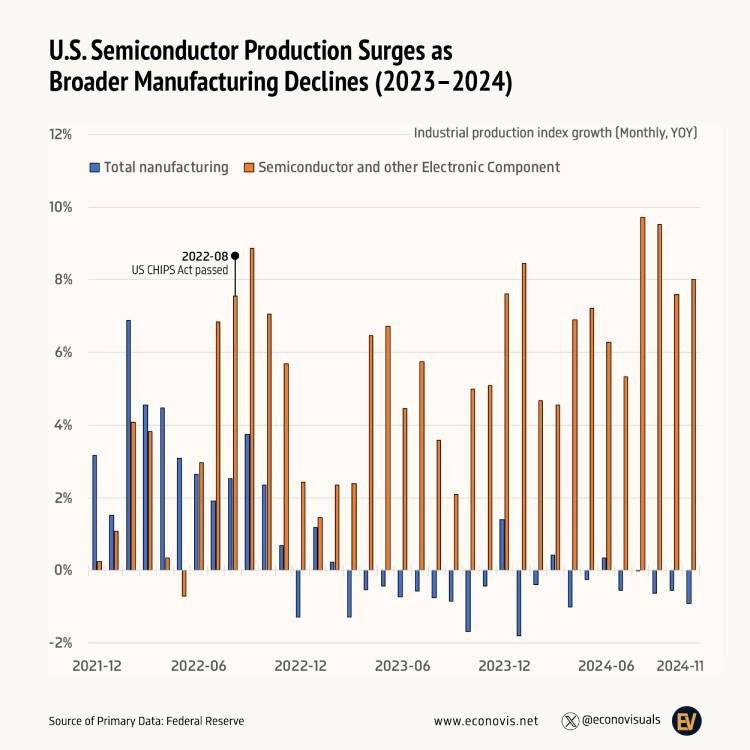

Graph showing U.S. semiconductor production growth compared to broader manufacturing trends (2023–2024). (Source: Econovisuals via X)

Meanwhile, US chip manufacturing capacity is expected to triple by 2032, according to a new report published by the Semiconductor Industry Association (SIA), which does indicate positive progress nearly two years after President Biden signed the CHIPS and Science Act into law.

That increase is expected to grow the US's share of global semiconductor production to 14% by 2032 from 10% today in a global bid to expand its chip manufacturing capacity to meet growing application demands, particularly in advanced semiconductors used for artificial intelligence.

The US has maintained a strong position in chip design and research and development led by companies like Intel and Nvidia, but it manufactures just 10% of the global chip supply. Meanwhile, 100% of all advanced chips are developed overseas, mostly by TSMC in Taiwan.

The concerns over supply difficulties that prompted the Biden administration to pass the $50 billion CHIPS Act in 2022, aimed at bringing manufacturing back to the US, certainly appears to have had the right effect. The incentives included in that package have attracted nearly half a trillion dollars in investments to build fabrication facilities in the US.

What about The USA's other thorny relationship, the one with Russia?

Russia’s Struggles in Semiconductor Manufacturing

In the succeeding decades following the fall of the USSR, imports accounted for virtually all of the country's microchips. The Soviet-era microelectronics industry could not compete with international manufacturers.

In the post-Soviet era, the legacy of outdated equipment and lack of skilled personnel continued to bedevil attempts by Russia to create a domestic, world-class chip industry.

Close-up of the Baikal Electronics BE-S1000 microprocessor die, manufactured using TSMC's 16nm process. (Image credit: Fritzchens Fritz, CC0, via Wikimedia Commons)

Mikron and Angstrem are Russia's only high performance chip fabricating companies. Its parent company, T Platforms, declared bankruptcy in 2023 and auctioned off its fabless chip design subsidiary (Baikal Electronics). It is thought that T Platforms failed because it relied on domestic technology. At its liquidation, the company was forced to repay a two-and-a-quarter billion-rouble subsidy.

Since 2010, its microelectronics industry has been built from scratch. Export controls, economic sanctions and isolation from international technology ecosystems have undercut the effort to establish a domestic and sovereign microchip industry. Vladimir Putin's security regime has created additional challenges. Restricted intellectual freedom and movement have put in motion an exodus of skilled scientists. Such policies will always inhibit the technology sphere.

These factors create serious difficulties for Russia's domestic chip industry. The fabrication process has a 50% defective rate. Such flawed quality control impacts the productivity of the entire industrial infrastructure. Russia now imports 90% of its computer chips from the People's Republic of China.

The importation of semiconductor material and fabrication equipment is half of what it was prior to the Ukrainian war but substantial. International collaboration is essential to the chip industry. If a Russian microprocessor developer were to find a foreign firm willing to risk sanctions and produce chips, it would require launching new production lines and cost the same as starting from the ground up. Building a microchip fabrication site costs time and money to coordinate designs, establish supply chains, and shed legacy architectures and components.

In addition to these challenges, Russia's central bank has raised interest rates to 21%. Profits do not cover the cost of loans. This means technology companies that pay high wage rates due to manpower shortages are trapped between an inability to finance high-tech equipment and long production cycles.

The Kremlin's solution looks to be providing more money to solve the problem. Since the imposition of sanctions, the Russian government has pledged to spend US$38 billion in its microchip industry by 2030.

In comparison, America's 2022 CHIPS and Science Act allocates US$280 billion to advance semiconductor research and manufacturing in the US. The legislation that includes a package of subsidies, tax credits, and grants for workforce development has already generated US$450 billion in private investments for US semiconductor production.

Europe’s Semiconductor Investments and Challenges

Where are Europe's chipmakers and governments in all of this? Many would say they are the weak link in the semiconductor chain, and there are a number of reasons for that.

Europe trails global rivals in technologies but does have advanced connectivity. In advanced manufacturing, health biotech, energy tech and space technologies Europe does well but is behind in AI and advanced semiconductors.

This could be partly due to inadequate public and private investment across several critical technologies. For example, private investment into AI start-ups and scale-ups in the EU is about one-seventh of that of the US, and about three times less than in the US for quantum computing.

However, Europe is outstanding in its research and development across many technology areas but the EU struggles to translate it into manufacturing and commercialisation. This limits the ability to capture the full economic value of these innovations within Europe.

But there is good news when it comes to European chip investment. The EU executive, which is hoping state subsidies will help the bloc achieve a 20% share of global chip capacity by 2030, came up with its proposal after a global chip shortage and supply chain bottlenecks hit car makers, healthcare providers and telecoms operators.

According to Reuters, Europe's share of chip production stands at 8%, down from 24% in 2000

Last November EU countries have agreed to a €43billion plan to fund the production of chips in the economic bloc. The move is part of the EU plan to lessen its dependence on chips made in Asia and the United States, and comes after the implications of chip shortages impacted on many European governments during the Covid-19 pandemic of 2020 and 2021.

To solve the chip crisis, the European Commission in February 2022 unveiled its multi-billion euro Chips Act to bolster the continent's competitiveness in the sector.

The EC plan had first been announced by Ursula von der Leyen back in 2021, when in March of that year, the European Union, under its 2030 Digital Compass plan, announced it wanted to produce at least 20% of the world's advanced semiconductors by 2030.

United Kingdom's Semiconductor Industry and Growth Potential

How is the UK doing in all of this? According to Tech UK, the UK's Technology Trade Association techUK, the global semiconductor market is huge and was valued at approximately $574 billion in 2022. The UK has a small percentage of this global market (1% - 1.5%).

So, the UK's semiconductor industry is relatively small compared to that of the US, the EU, and other Asian countries. Furthermore, the UK does not have an end-to-end supply chain for semiconductors, making it susceptible to supply chain disruptions. However, despite its small overall size, the UK semiconductor sector has significant academic and industrial know-how in complementary metal oxide semiconductor (CMOS) post-processing and innovative chip architectures.

The industry has strong capabilities in various packaging technologies, including radio frequency and power, and plenty of knowledge in advanced heterogeneous 2.5D/3D packaging technologies. The UK is also skilled in compound semiconductor materials, processes, chip design and intellectual property across various applications.

Major Challenges Ahead

It's crucial to address the key challenges that hinder the UK's ability to build a competitive semiconductor industry. These challenges include skills shortages. The sector requires a diverse range of specialist skills, but unfortunately, some of these skills are in extremely short supply in the UK.

Another difficulty is the lack of adequate allocation of resources and investment, and there is currently an imbalance between capital for scaling-up and R&D investment in the UK to support next-generation compound semiconductor and packaging developments, with most of the investment allocated to R&D. The risk is that without scaling-up support, users will be driven towards overseas suppliers.

The UK semiconductor industry also lacks adequate facilities for silicon processing. To increase collaboration with high-volume production foundries abroad is necessary. This requires the use of compatible processes and materials.

Finally, a lack of a secure supply of certain critical semiconductor materials used as basic materials for packaging hinders manufacturing. As a result, there is no source for silicon carbide (SiC) substrates in the UK, and there are currently US export control restrictions for the same material. This leads to long lead times for material delivery and variations in quality.

However, there are positive opportunities for growth in the UK. It has some of the finest semiconductor companies in the world. And although the UK accounts for a very small percentage of sales of semiconductors across the world, its products have global reach (over 90% of silicon semiconductors created in the UK are exported).

Furthermore, the UK has strong capabilities in IP and chip design, compound semiconductors and R&D. It also has world-class universities and research activities on different materials and technologies like silicon and compound processes, advanced packaging processes and novel chip architectures.

So there's good reason for the UK to be optimistic.

Who Will Dominate Global Chip Supremacy in 2025?

It's pretty much impossible to be 100% certain on such a prediction but my money goes on a combination of the major players that will outstrip all others when it comes to developing leading-edge semiconductors and being able to produce them in high quantities.

So, for me, Taiwan, in cooperation with the US, will be the one to lead the charge. It's clear that the US wants Taiwan's chip makers to establish more of their fab facilities in the USA, and plans to implement this have already succeeded. America itself has big investment projects for its domestic manufacturers, and these are showing very positive results. In addition to America, Taiwan is also spreading its manufacturing bases into Japan, and because this trio of countries can work well together, I see the chip products that they will create as being the most desirable in the world.